If you are a high-earning physician, specialist, or successful business owner in the United States, you likely already work with a CPA firm. Your certified public accountant prepares your tax return, ensures your tax compliance, and keeps your financial accounting in order. You may also work with a financial advisor to manage investments and wealth accumulation. On the surface, everything appears structured and responsible.

Yet every tax season, when the numbers are finalized, many professionals still feel the sting of an unexpectedly high tax bill. The frustration is not about accuracy. It is about tax liability. Despite strong income and careful accounting, your taxable income remains high, and your overall tax strategy feels reactive instead of intentional.

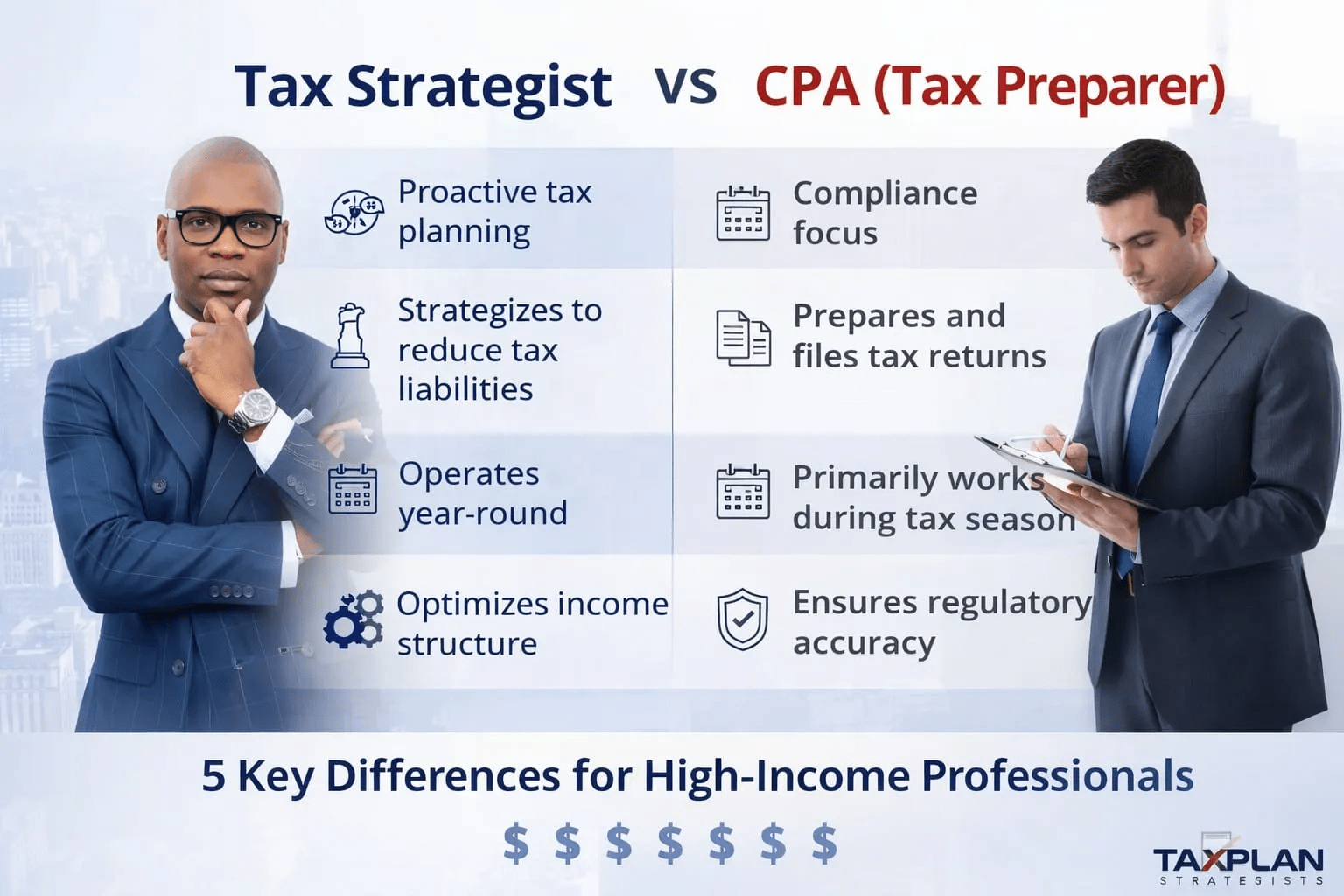

The issue is rarely incompetence. It is role clarity. A CPA, public accountant, or tax preparer is trained primarily in compliance and reporting under current tax law. A tax strategist, however, focuses on proactive tax planning designed to reduce tax liability before the year closes. That distinction has meaningful financial consequences.

Schedule Your Free Consultation!

Compliance Is Necessary. Strategy Is Transformational.

A certified public accountant completes rigorous education, passes the CPA exam, and operates under the oversight of a state board. Their expertise lies in accounting, auditing, financial reporting, and proper tax preparation. CPA firms provide essential tax services that protect clients from penalties and ensure documentation aligns with federal and state regulations.

However, compliance answers the question, “What happened last year?” It documents income, applies deductions, and calculates what is owed. By the time the tax return is prepared, most structural decisions have already been finalized.

A tax strategist operates differently. Instead of reacting during tax season, a tax strategist focuses on year-round planning. That means evaluating entity structure, modeling taxable income projections, coordinating retirement contributions, and adjusting compensation strategy before deadlines eliminate flexibility. The difference between tax compliance and proactive tax planning often determines whether a professional pays the minimum legally required or significantly more.

The April Reaction Cycle

Many high-income professionals operate in what can be described as an April Reaction cycle. Throughout the year, they grow revenue, manage customers, oversee marketing initiatives, and focus on business administration. A business owner may invest in customer acquisition campaigns, test Google Ads strategies, or expand through acquisition. These decisions affect cash flow and long-term wealth building.

Then tax season arrives. The tax preparer compiles documentation, calculates deductions, and presents the final tax bill. At that stage, there is little room for adjustment. Income has already been earned. Taxable income has already been determined. Tax implications have already been locked in.

Strategic planning, by contrast, occurs before those outcomes are fixed. It anticipates revenue increases, evaluates entity elections, adjusts compensation structures, and coordinates planning across accounting systems and information systems so that decisions align with a broader tax strategy. This proactive approach transforms tax planning from an annual event into an integrated financial strategy.

CPA Firms and Tax Strategists Serve Different Roles

There is a misconception that hiring a tax strategist replaces your CPA firm. In reality, the two roles are complementary. CPA firms focus on financial accounting, tax preparation, and compliance under tax law. A tax strategist focuses on reducing tax liability through intentional structure.

When comparing a tax strategist vs CPA, consider the scope. A CPA ensures the books are accurate and compliant. A tax strategist evaluates whether the structure itself is optimized. In many cases, this involves working alongside a financial advisor, reviewing business structure, and coordinating tax advice with long-term wealth protection goals.

Compliance protects you from penalties. Strategy protects you from overpaying.

Why High-Earning Professionals Feel the Gap

For a high-income business owner or medical professional, income is rarely simple. You may receive W-2 compensation, 1099 income, partnership distributions, and real estate revenue. Each stream carries different tax implications under United States tax law.

Without proactive tax planning, these streams are simply aggregated and reported. With planning, they are structured intentionally. Decisions about salary versus distributions, retirement plan design, and entity classification directly affect taxable income and overall tax liability.

Over time, reducing taxable income strategically can significantly increase retained wealth. Even modest improvements in effective tax rate can improve cash flow, strengthen long-term planning, and accelerate wealth accumulation.

What Real Tax Strategy Looks Like

Effective tax strategy is not about aggressive loopholes. It is about disciplined planning within the framework of existing tax law. It may involve timing income recognition, maximizing legitimate deductions, restructuring compensation, or aligning retirement contributions with projected income.

It also involves coordination. Many professionals rely on multiple advisors who operate in silos. A financial advisor focuses on investments. A CPA focuses on compliance. A managing partner within a firm may focus on growth and marketing strategy. Without integration, tax planning becomes fragmented.

A tax strategist ensures that accounting decisions, marketing campaigns, expansion initiatives, and compensation structures align with a cohesive plan. Whether you are launching social media campaigns for customer acquisition or scaling through strategic acquisition, each growth decision should be evaluated for its tax implications before it affects your tax liability.

Tax Strategies at Legally Mine!

The Cost of Staying Reactive

Remaining in compliance mode is comfortable because it is familiar. Accounting today, as a profession, has historically emphasized accuracy and reporting. That foundation is important. But for high earners, compliance alone often leaves opportunity on the table.

Every year that proactive planning is absent represents potential overpayment. That excess tax bill is not just a one-time expense. It reduces reinvestment capacity, limits wealth growth, and constrains future strategy.

Strategic tax planning is about positioning. It is about aligning tax services with broader financial objectives. It is about ensuring that growth, marketing, expansion, and operational decisions reflect intentional design rather than after-the-fact adjustments.

Building the Right Advisory Team

The goal is not to dismiss your CPA or tax preparer. A certified public accountant plays a critical role in financial accountability and auditing standards. Tax preparation and tax compliance are non-negotiable.

However, high-income professionals benefit from layered expertise. A tax strategist focuses on reducing tax liability before tax season. A financial advisor supports long-term wealth development. CFO services may support forecasting and cash flow modeling. Together, these roles create a comprehensive structure that aligns business growth with intelligent planning.

For new customers seeking clarity, the key takeaway is simple: compliance files your return. Strategy designs your outcome.

If you want to move beyond reacting to your tax bill and begin implementing a proactive tax strategy designed to reduce taxable income and protect wealth, schedule your free consultation with Legally Mine today.

Frequently Asked Questions

What is the difference between a CPA and a tax strategist?

A certified public accountant focuses on tax compliance, financial accounting, auditing standards, and preparing your tax return in accordance with current tax law in the United States. A tax strategist focuses on proactive tax planning throughout the year. Instead of reporting what already happened, a tax strategist designs a forward-looking tax strategy to reduce tax liability and optimize taxable income before deadlines pass.

Do I still need a CPA firm if I hire a tax strategist?

Yes. A CPA firm handles accounting, documentation, and tax preparation to ensure compliance. A tax strategist works alongside them to reduce tax liability through intentional planning. The roles are complementary: compliance files the return, while strategy shapes the outcome.

When should tax planning happen?

Tax planning should occur year-round, not just during tax season. Once your tax return is being prepared, most structural decisions are already locked in. Proactive planning evaluates projected taxable income, deductions, entity structure, and compensation strategy while there is still flexibility to adjust and reduce your tax bill.

How does proactive tax strategy reduce taxable income?

A proactive tax strategy reduces taxable income by aligning structure, timing, and compensation decisions with tax law. For a business owner, decisions related to expansion, acquisition, marketing campaigns, and cash flow all carry tax implications. Evaluating those decisions in advance allows for measurable reductions in overall tax liability.

Can tax strategy improve long-term wealth growth?

Yes. Lowering tax liability increases retained capital, strengthens cash flow, and accelerates wealth accumulation. Over time, strategic tax planning can have a significant impact on long-term financial outcomes.

Is tax strategy only for large firms?

No. While managing partners and larger firms often use strategic tax planning, high-earning professionals and growing businesses benefit just as much. Any business owner seeking to move beyond basic tax services and into intentional financial strategy can benefit from working with a tax strategist.

About Legally Mine

Legally Mine is a leading asset and lawsuit protection company that helps businesses and professionals proactively manage risk. Through specialized consulting and proven legal structures, Legally Mine provides practical tools to protect personal and business assets, reduce liability exposure, and give owners peace of mind, so they can focus on running their business with confidence.