Most physicians spend years building a practice worth protecting as part of a long-term wealth protection strategy. Yet a significant number of those same physicians rely on a basic will as the foundation of their estate planning strategy. A will is better than nothing, but for a physician it creates a gap that can cost your family, your staff, and your patients far more than you realize and leaves your personal asset protection completely exposed.

That gap is probate. And the most reliable tool to close it is a living trust.

This guide explains how probate specifically threatens a medical practice, why a living trust is the most effective solution for probate avoidance, and what physicians should know before updating their plan.

What Probate Actually Does to a Medical Practice

Probate is the court-supervised process of settling a deceased person’s estate. For most people, it means delay and legal fees. For a physician who owns a practice, it means something much more disruptive.

When a physician dies with only a will in place, the practice does not automatically transfer to anyone. Before assets can move, the court must validate the will, appoint an executor, notify creditors, and give the public an opportunity to file claims. In most states, this process takes six months to two years.

During that window, the following can happen:

- The practice license goes dark. The physician who held the license is gone, and no clear legal authority exists to operate under that license until probate closes.

- Patients lose their provider. Without continuity, patients seek care elsewhere. Some will not return.

- Staff face payroll uncertainty. Without a functioning entity to process payroll, employees make decisions about their own financial security.

- A competitor can move in. Probate is a public process. Other practices in your area will know your practice is in limbo, and some will recruit your patients and staff accordingly.

A living trust bypasses all of this. Assets held inside the trust transfer immediately to your named successor trustee at death, with no court involvement required. The practice keeps operating. Payroll continues. Patients are covered.

See How Legally Mine Can Help You

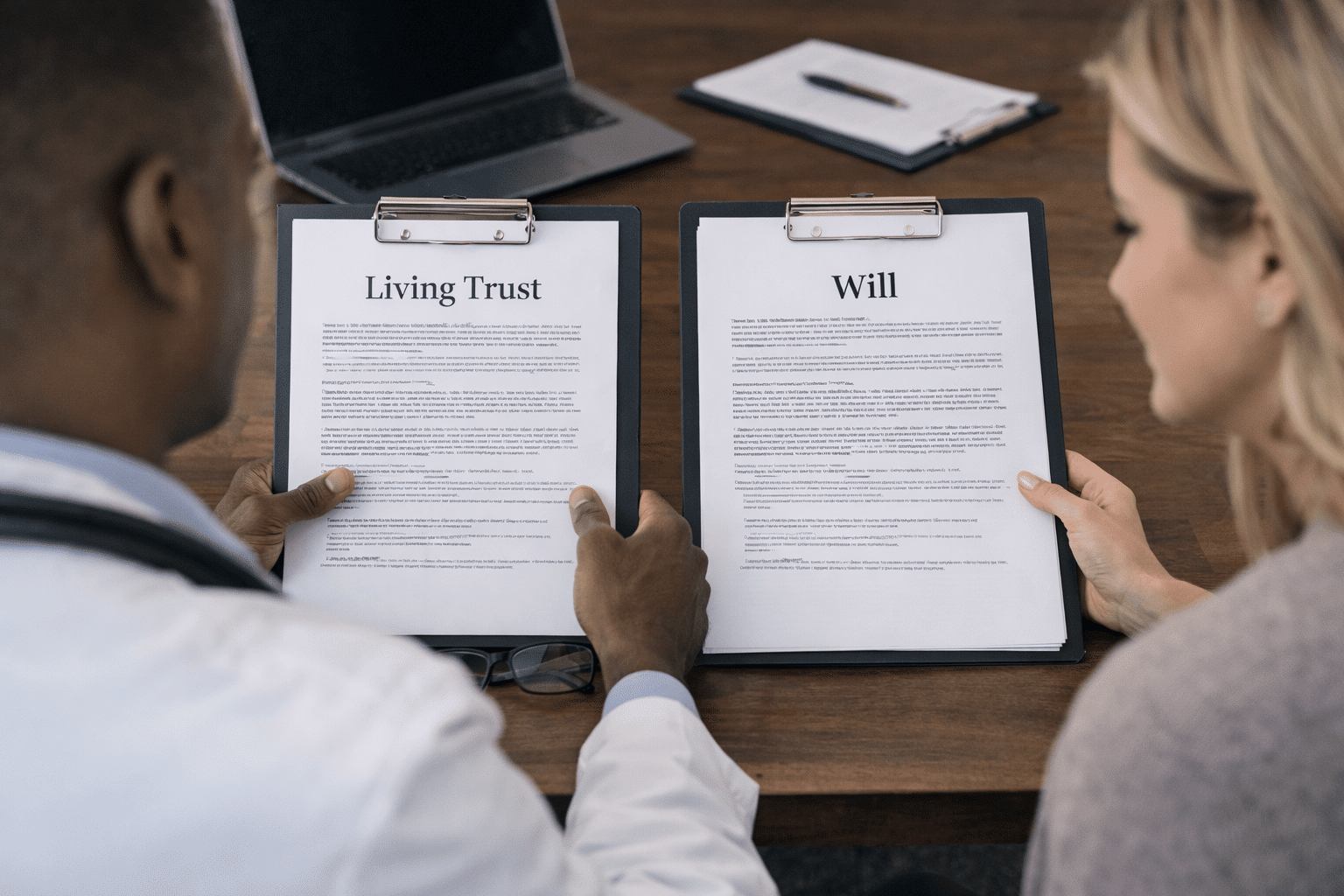

Living Trust vs. Will: The Core Difference for Physicians

Both a living trust and a will express your wishes for how your assets should be distributed. The difference is in how and when those wishes take effect.

A will only takes effect at death and only after probate validates it. A living trust takes effect the moment you sign it and transfer assets into it. You remain in full control as the trustee during your lifetime. At incapacity or death, the successor trustee you named steps in immediately, without any court proceeding.

For estate planning purposes, this difference is significant across three areas:

1. Speed of Transfer

A living trust can transfer a medical practice, real estate, investment accounts, and other assets within days of death. Probate takes months to years. For a practice that depends on daily operations to hold its value, speed matters.

2. Privacy

Wills become public record once they enter probate. A living trust does not. For physicians with professional liability exposure, creditors, or business partners, keeping the details of your estate private is a meaningful element of wealth protection. Privacy is a foundational element of personal asset protection for any high-earning professional.

3. Multi-State Coverage

If you own real estate or practice in more than one state, a will requires a separate probate proceeding in each state. A living trust covers all of those assets under one document, regardless of state lines.

Schedule Your Free Consultation

A living trust does not replace a will entirely. You still need a pour-over will as a backstop for any assets not transferred into the trust during your lifetime. The two documents work together as part of a complete estate planning strategy.

Personal Asset Protection and Professional Liability

Physicians carry a level of professional liability exposure that most professionals do not. A malpractice claim, a billing dispute, or an employment-related lawsuit can emerge years after the underlying incident. Estate planning that does not account for this exposure is incomplete.

A revocable living trust does not, on its own, protect assets from creditors during your lifetime. Because you retain control as trustee, courts generally treat the trust assets as still accessible to creditors. This is an important distinction that many physicians miss.

Effective personal asset protection for a physician typically involves layering additional structures alongside a living trust. These include:

- Professional entities (PC or PLLC): Separating practice liabilities from personal assets.

- Irrevocable trusts: Assets transferred into an irrevocable structure are generally outside the reach of future creditors, subject to applicable fraudulent transfer rules.

- Holding companies and LLCs: Effective for managing investment real estate or business interests separately from your personal balance sheet.

- Umbrella and malpractice insurance: Your first line of defense in any wealth protection plan and a necessary part of any complete strategy.

The living trust provides probate avoidance, privacy, and continuity. The broader asset protection layer addresses creditor protection and lawsuit protection during your lifetime. A sound wealth protection strategy requires both.

For more detail on how professional liability intersects with physician estate plans, the American Medical Association and White Coat Investor both publish resources relevant to physician-specific risk exposure.

Explore Asset Protection Strategy Options at Legally Mine!

Reducing Tax Burden Through Proper Trust Structure

A living trust is tax-neutral during the grantor’s lifetime. It does not reduce your taxable income or shield assets from estate taxes on its own. However, the way assets are structured inside and around a living trust can significantly affect your tax position.

Several planning tools used alongside a living trust can help with reducing tax burden:

- Charitable remainder trusts (CRTs): Donate appreciated assets, receive an income stream, and generate a charitable deduction. How charitable donations affect taxes depends on the structure, but CRTs can be a meaningful part of a high-earner’s plan.

- Spousal Lifetime Access Trusts (SLATs): A way to remove assets from your taxable estate while still allowing a spouse access.

- Annual gifting strategies: The annual gift tax exclusion and lifetime exemption should both be reviewed as part of your plan, particularly given ongoing legislative uncertainty around estate tax thresholds.

Physicians looking to understand how to reduce taxable income for high earners, how to lower taxable income, or how to maximize tax deductions should work with both a tax advisor and an estate planning attorney. These are coordinated decisions that form the backbone of personal asset protection for higher earners, not separate ones. The IRS Newsroom is a reliable resource for tracking current contribution limits and estate tax thresholds.

Explore Tax Strategy Options at Legally Mine!

Does Probate Avoidance Work the Same in Every State?

No, and this matters for physicians who practice across state lines or own real estate in multiple states.

Each state has its own probate rules, timelines, and thresholds. Some states have simplified procedures for smaller estates. Others have lengthy and expensive processes. A living trust provides consistent probate avoidance across all states because trust assets do not pass through any state’s probate system.

It is worth noting that some states have community property rules that affect how assets held in a living trust are treated at death. If you have recently moved, married, or acquired property in a new state, your estate planning documents should be reviewed by an attorney licensed in that state to ensure your wealth protection strategy holds up across jurisdictions.

Mercer Advisors and Morgan Lewis have both published analysis on how estate planning intersects with state-specific rules for high-net-worth professionals. See Mercer Advisors and Morgan Lewis for additional context.

Frequently Asked Questions

Does a living trust provide probate avoidance for a medical practice?

Yes, but only for the assets that are actually titled into the trust. The practice entity, equipment, accounts, and intellectual property all need to be properly transferred. A living trust that is not fully funded at the time of death will leave those unfunded assets subject to probate. This is one of the most common and costly errors in physician estate plans.

What is the difference between probate avoidance and creditor protection?

Probate avoidance means your assets transfer to heirs without going through the court process. Creditor protection is the cornerstone of personal asset protection, meaning certain assets are shielded from claims by future creditors or plaintiffs. A revocable living trust provides the first. It does not, on its own, provide the second. Full personal asset protection for a physician with professional liability exposure requires additional structures layered into the overall estate planning strategy.

How does professional liability exposure affect my estate plan?

Physicians are at higher risk of civil judgments than most professionals. A malpractice claim can follow an estate through probate if it was filed before death. Wealth protection strategies that combine a living trust with appropriate liability structures reduce the window during which a claim can attach to your personal assets. This is why estate planning and personal asset protection need to be coordinated into a unified wealth protection plan, not treated as separate exercises.

Does probate avoidance work the same in every state?

No. Probate rules, timelines, and fees vary significantly by state. A living trust provides consistent probate avoidance across all states because trust assets never enter the probate system. For physicians with property or practice locations in multiple states, a living trust is especially important to avoid multiple simultaneous probate proceedings.

What is the fastest way to set up a probate avoidance plan as a physician?

The fastest path is to schedule a consultation with an estate planning attorney who has specific experience working with medical professionals. A living trust can typically be drafted and executed within a few weeks. The more time-consuming step is funding the trust: retitling real estate, updating beneficiary designations, and transferring practice assets. Starting that process now, even if your estate planning feels less urgent, is the most effective form of wealth protection available to you.

Ready to Close the Gap in Your Estate Plan?

A living trust is one of the most effective tools available for probate avoidance, practice continuity, and wealth protection. If you are a physician who currently relies on a will alone, or whose estate planning documents have not been updated in the last three to five years, now is the time to review your plan.

Legally Mine works with physicians, dentists, and surgeons to build personal asset protection strategies that go beyond the basics. Our team understands the specific risks created by professional liability exposure and builds plans designed to protect your practice, your family, and your wealth for the long term.

About Legally Mine

Legally Mine is a leading asset and lawsuit protection company that helps businesses and professionals proactively manage risk. Through specialized consulting and proven legal structures, Legally Mine provides practical tools to protect personal and business assets, reduce liability exposure, and give owners peace of mind, so they can focus on running their business with confidence.

Disclaimer

The information provided on this website does not constitute legal advice or tax advice. Customers of Legally Mine have no attorney-client privilege with representatives of Legally Mine, and no confidential relationship exists or will be formed by using its services. For personal legal or tax advice, please consult a licensed attorney or personal accountant.