Most high-earning medical professionals spend years building something extraordinary: a practice, a reputation, a life. But somewhere between the long hours and hard work, a quiet leak opens in their finances. Not from lawsuits. Not from bad investments. From overpaying taxes, year after year, because no one on their team was built to stop it.

The tax burden for medical professionals is one of the most preventable financial threats in their careers. And yet, the majority continue overpaying not out of carelessness, but because the system they’ve been handed was never designed to advocate for them.

This post is about what changes when that stops.

Schedule Your Free Consultation

“It Is Every American’s Duty Not to Overpay Taxes”

That quote is often attributed to Judge Learned Hand, one of the most respected judicial voices in American legal history. It’s not a loophole philosophy. It’s not aggressive accounting. It’s a principle baked into tax law itself.

The IRS doesn’t reward overpayment. It doesn’t penalize legal proactive tax planning. What it penalizes is non-compliance and that’s an entirely different conversation.

The distinction matters because one of the biggest mental barriers keeping high earners from implementing a real tax strategy is the belief that doing so invites scrutiny. That if you start reducing your taxable income too intentionally, you’re waving a red flag.

That belief is costing you money every single year.

Learn More About Tax Strategies

Before and After: Real Scenarios, Real Results

These scenarios are based on strategies that are fully legal, IRS-compliant, and available to most medical and business professionals right now. The numbers reflect real outcomes grounded in established tax strategy.

The Physician Paying Himself the Wrong Way

Before: Dr. Reyes is an orthopedic surgeon earning $450,000 per year as a sole proprietor. He pays self-employment tax on his full net income. His income tax obligations, combined with federal and state liability, leave him writing large checks to the IRS each tax season. His CPA files everything correctly but no one has asked the right question: is this the right structure for wealth management?

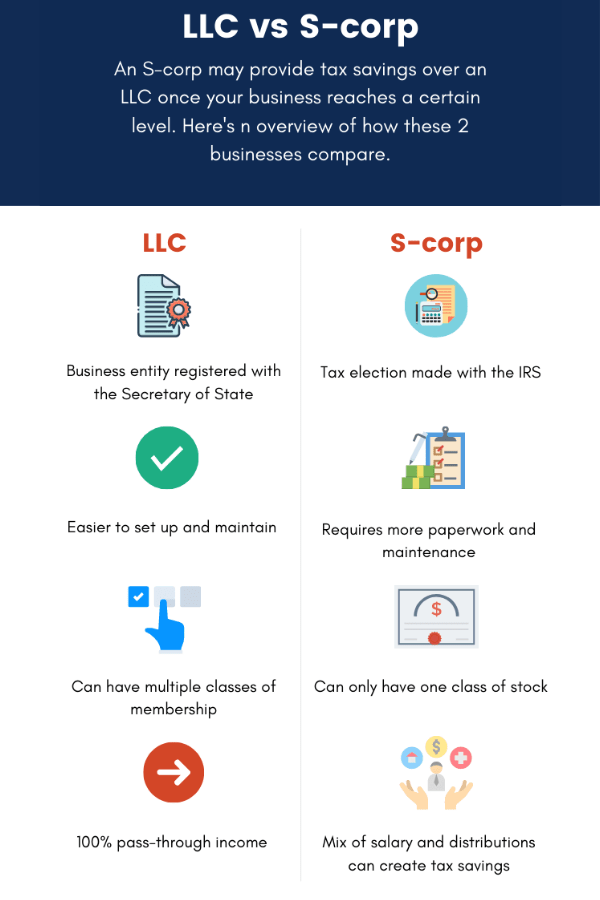

The Strategy: An S-Corporation election.

By restructuring and paying himself a “reasonable salary” say, $180,000 and distributing the remainder as shareholder income, Dr. Reyes removes a significant portion of his earnings from FICA and self-employment tax exposure. That distribution is not subject to the 15.3% self-employment tax applied to his full salary.

After: Same income. Significantly lower tax liability. Savings often range between $20,000 and $40,000 per year depending on income level. That’s not a tax benefit reserved for the ultra-wealthy. That’s financial planning through correct structuring.

Explore Tax Strategy Options at Legally Mine!

The Practice Owner Who Didn’t Know About the Augusta Rule

Before: Dr. Kim owns a growing dental practice and regularly hosts business planning meetings at her home. She’s never thought to treat those meetings as part of her proactive tax planning or to document them as a legitimate business event with real financial implications.

The Strategy: IRC Section 280(a) commonly called the Augusta Rule.

Under this provision, a business can rent a personal residence for up to 14 days per year. The business deducts the payment as a legitimate expense. The individual receives it as non-taxable income. When applied correctly with proper documentation, this is a clean, IRS-recognized strategy that reduces taxable income for the business while putting tax-free dollars in the owner’s pocket.

After: Dr. Kim’s business now pays her a fair market rental rate for six documented business meetings per year. At $1,500 per day, that’s $9,000 in tax-free income and a corresponding business deduction from a space she was already using. That’s tax efficiency at its most straightforward.

See How This Strategy Could Work for You

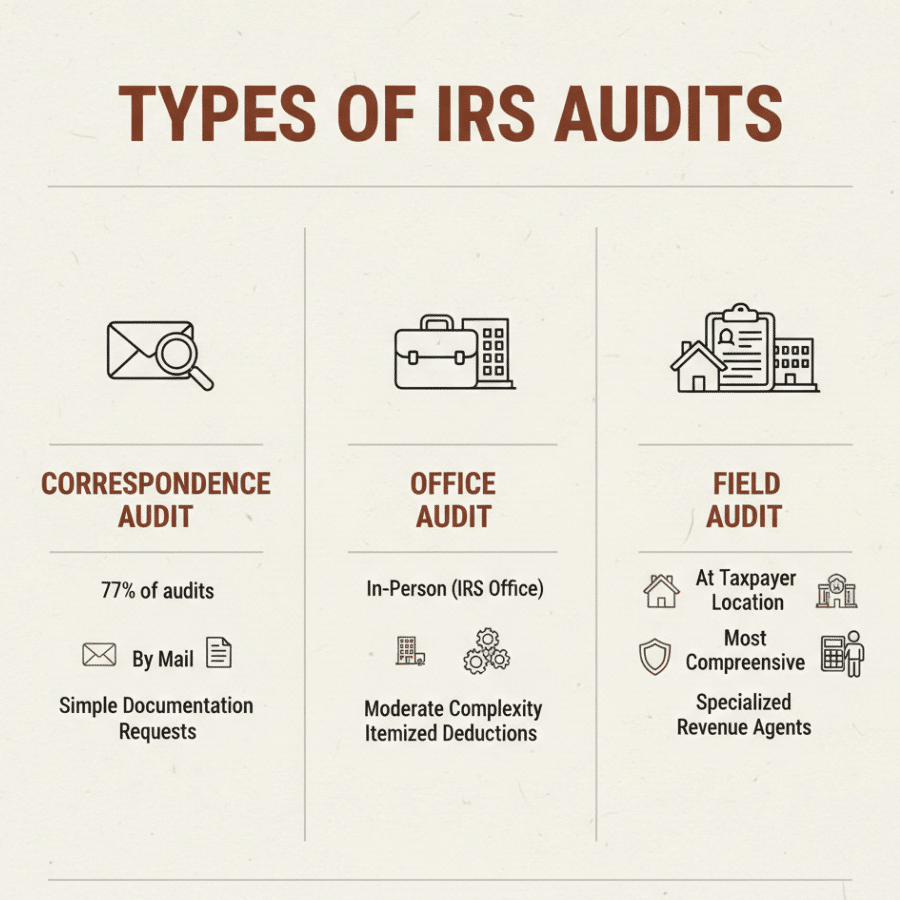

The Audit Question: Let’s Actually Answer It

Here’s the honest answer about IRS audits and advanced tax planning: the IRS flags inconsistency, missing documentation, and structural red flags not well-executed legal strategy.

A correctly structured S-Corp with appropriate salary documentation does not invite scrutiny. A properly executed 280(a) rental arrangement with fair market value records and written agreements does not trigger concern. In fact, correct entity structuring reviewed by a state-licensed tax professional and attorney tends to increase compliance, not reduce it.

What Actually Puts You at Risk

Professionals who face audit risk are typically those who claim deductions without documentation, misclassify employees, or apply tax laws outside their legal structure. A proactive tax plan from Legally Mine is designed to build a structure so clean, so documented, and so legally sound that it holds up under any review.

The goal is never to hide. The goal is to ensure every dollar you’re entitled to keep is properly protected and every deduction you claim has a foundation that would satisfy any examiner.

What Correct Structuring Actually Looks Like

Every plan Legally Mine implements is reviewed by a state-specific licensed attorney. That means the strategies applied to your income, your assets, and your retirement planning aren’t generic. They’re designed for the legal environment where you actually practice and built to withstand scrutiny at the federal and state level.

Talk to a Tax Strategist Today

What Changes: The Full Picture of Wealth Preservation

The financial results are real. But for most professionals who implement a proactive plan, the transformation goes beyond numbers on a tax return.

Confidence Replaces Anxiety

One of the most consistent responses from medical professionals who work with Legally Mine is the relief that comes from finally understanding their own structure. When you know your entities are correctly formed, your strategies are documented, and your financial goals are being actively pursued rather than accidentally missed, the ambient stress disappears.

Strategy Becomes Intentional

Before implementing a proactive plan, many professionals describe their tax situation as something that happens to them each tax season. After, it becomes something they actively direct in partnership with a team built around their interests, not just their filings.

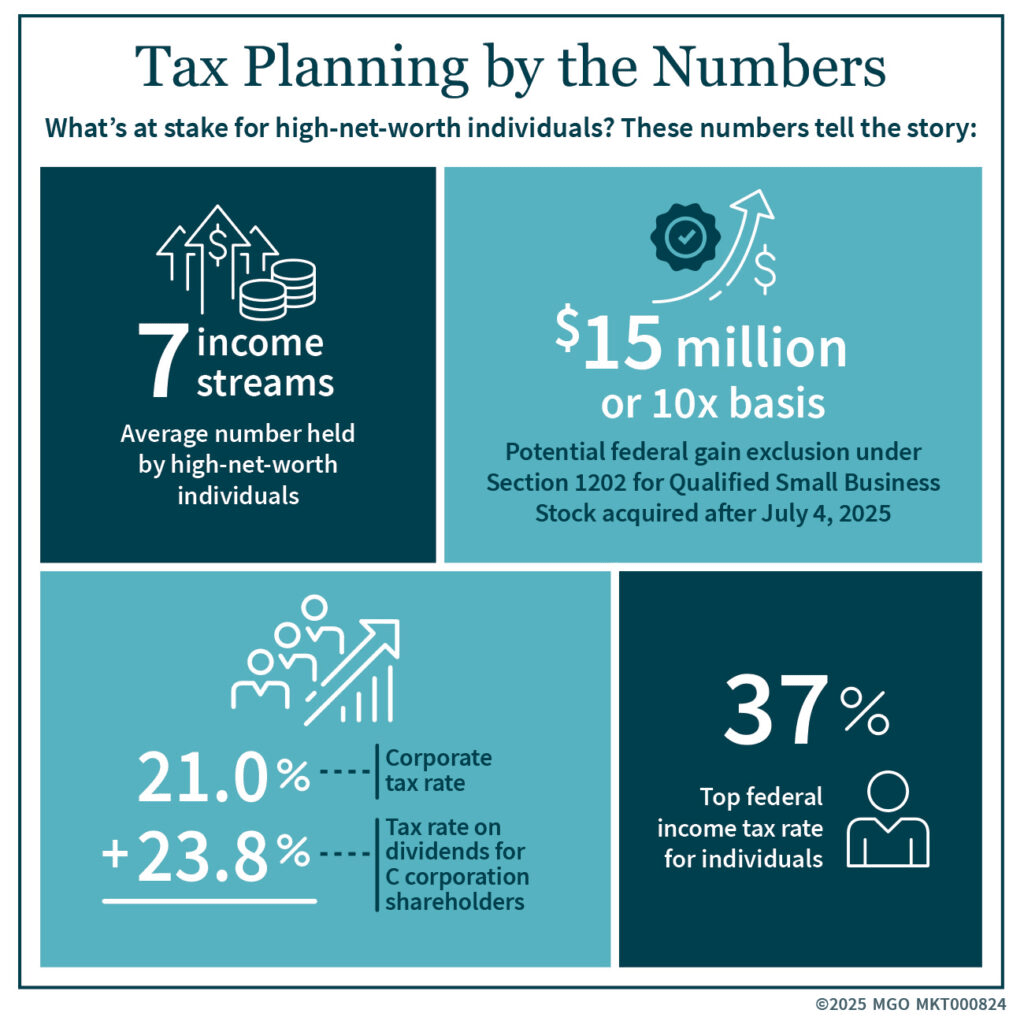

This shift applies across the full spectrum of wealth protection: asset protection, income tax strategy, capital gains tax planning, estate taxes, and retirement income planning all become part of a coherent, connected system.

Your Savings Compound Over Time

An S-Corp election that saves $30,000 this year saves $30,000 next year, and the year after that. A Roth IRA or Roth conversion strategy implemented at the right time can protect decades of investment growth from future income tax. A properly structured estate plan including tools like a family limited partnership or charitable remainder trust means those savings eventually flow to your heirs and your generational wealth goals without unnecessary loss to estate taxes or federal estate tax exposure.

The strategies are designed to work together. Asset protection, tax optimization, financial planning, and estate planning aren’t three separate conversations at Legally Mine; they’re one integrated system.

Your Plan Stays Current

Tax laws change. Entity requirements evolve. The Big Beautiful Bill Act and ongoing updates to capital gains tax rules mean that a plan optimized in 2022 may need meaningful updates today. Legally Mine builds regular plan reviews into its model so clients aren’t left holding a strategy that’s no longer doing its job.

Request Your Consultation Now!

How Much Could You Realistically Save?

This is the question everyone wants answered and the honest answer is that it depends on your income, your current structure, and how many strategies are currently underutilized.

What We Can Say With Confidence

Medical professionals earning $300,000 or more per year regularly see annual tax savings of $20,000 to $50,000 through proper S-Corp structuring and targeted deduction strategies. Professionals who implement a layered approach combining S-Corp elections, the Augusta Rule, tax-advantaged account optimization, and retirement planning often see significantly more.

Legally Mine guarantees that identified tax savings will exceed the cost of its services or it refunds the difference. That’s the standard the firm holds itself to.

Common Strategies That Drive Real Results

Proactive tax planning isn’t one move. It’s a coordinated approach that may include some or all of the following, depending on your situation:

- S-Corporation election to reduce FICA and self-employment tax on distributions

- IRC Section 280(a) home rental for legitimate business deduction

- Tax loss harvesting to offset capital gain exposure in investment portfolios

- Roth conversion strategies to shift assets out of taxable income territory in lower-earning years

- Retirement planning structures that maximize tax-advantaged account contributions

- Estate planning tools including charitable giving strategies and life insurance structures that protect wealth across generations

- Capital gains tax planning for professionals with real estate holdings or investment portfolios

- Entity restructuring to create legal firewalls between personal assets and business liability

Find Out What You Could Be Keeping

Timing: Is It Too Late to Start?

For This Tax Year

Some strategies like an S-Corp election or a properly documented 280(a) arrangement can produce results within the same tax year they’re implemented. Others have mid-year or end-of-year deadlines. If you’re reading this now, there is likely still time to reduce your tax liability before the current year closes.

For Future Years

Even if the tax year has already ended, structural changes implemented now will significantly reduce your burden going forward. A Roth conversion, a revised entity structure, a formalized charitable giving strategy these are forward-looking tools that start working from the day they’re implemented.

The Real Cost of Waiting

The professionals who wish they had started sooner are almost universally the ones who waited for a triggering event: a large tax bill, a lawsuit scare, or a conversation with a colleague who’d just discovered how much they’d been overpaying. The best time to build a solid financial planning foundation is before you need it urgently. The second-best time is right now.

Schedule Your Free Consultation

The Only Thing Left Between You and This Outcome

The professionals in these scenarios weren’t uniquely strategic. They weren’t operating in gray areas of the tax code. They simply found an advisor whose entire model was built around helping them keep what they earn.

That’s what Legally Mine does not for a general clientele, but specifically for medical professionals, dental professionals, and business owners who have worked too hard to let their wealth preservation go unmanaged.

The only thing standing between where you are and where these professionals are is a conversation. Schedule your free consultation with Legally Mine today and find out exactly how much you could be keeping.

Frequently Asked Questions

How much money can a medical professional realistically save with a proactive tax plan?

Savings vary based on income, current structure, and which strategies are available to you. Medical professionals earning $300,000 or more per year commonly see annual tax savings of $20,000 to $50,000 or more through proper S-Corp structuring and targeted deduction strategies. Legally Mine guarantees that identified tax savings will exceed the cost of its services.

Will using advanced tax planning strategies increase my risk of an IRS audit?

No when strategies are correctly structured, fully documented, and legally compliant, they do not increase audit risk. The IRS flags inconsistency and missing documentation, not well-executed legal strategy. Every Legally Mine plan is reviewed by a state-licensed attorney to ensure it holds up to scrutiny.

How long does it take to see results after implementing a new tax strategy?

Some strategies produce results within the same tax season they’re implemented. Full structural implementation, including entity formation and estate planning documents, typically takes three to six months. That timeline reflects the thoroughness required to build something that lasts and holds up under review.

Is it too late in the year to start a proactive tax plan?

Not usually. Mid-year implementation can still capture meaningful savings for the current year, especially for deduction-based strategies. Even if the tax year has closed, forward-looking structural changes will significantly reduce your financial burden starting now. The best time to start is before you need it. The second-best time is today.

About Legally Mine

Legally Mine is a leading asset and lawsuit protection company that helps businesses and professionals proactively manage risk. Through specialized consulting and proven legal structures, Legally Mine provides practical tools to protect personal and business assets, reduce liability exposure, and give owners peace of mind, so they can focus on running their business with confidence.

Legally Mine has protected the assets and reduced the tax liability of more than 15,000 medical professionals nationwide. To learn what a proactive plan could mean for your financial future, schedule your free consultation today.