If you’re a physician earning $200,000 or more, chances are you already have a CPA. Your tax return is filed on time, your IRS tax forms are accurate, and you remain compliant with the Internal Revenue Service.

And yet, every year, you write a significant check and wonder:

“Am I paying more in taxes than I should?”

That question sits at the heart of the discussion around tax planning vs tax preparation. While most professionals assume they’re receiving comprehensive tax help, what they are actually getting is often limited to compliance. Your CPA files your taxes, but filing your taxes is not the same as reducing them.

Schedule Free Consultation with Legally Mine Now!

The Real Problem: Compliance Isn’t Optimization

Most tax professionals are trained to ensure your filings are accurate and compliant with current tax law. That role is essential. Without it, you could face penalties, a tax audit, or even more serious tax problems such as tax debt or a tax lien.

However, compliance is inherently backward-looking. It focuses entirely on what has already happened during the tax year. By the time your return is prepared, your financial outcome is largely locked in.

This is why many high-income earners feel stuck in a cycle where increased income leads to an increased tax liability, without any clear path to improvement. Even if you’ve never faced a major tax problem, the lack of proactive planning can quietly cost you thousands or even tens of thousands of dollars over time.

Understanding the 3 Layers: A Simple Framework

To fully understand tax planning vs tax preparation, it helps to break the system into three distinct layers. Each layer plays a different role, but most professionals only engage with the first.

Tax Preparation: Reporting the Past

Tax preparation is the annual process of filing your tax return and ensuring compliance with federal and state requirements. This includes completing IRS tax forms, organizing financial records, and addressing any immediate tax issue that may arise.

It becomes especially important if you’re dealing with complications such as an unfiled tax return, non filed tax returns, or situations requiring IRS audit assistance or tax resolution services. In those cases, preparation and tax resolution help correct existing tax problems and restore compliance.

But even when done perfectly, tax preparation does not reduce your taxes after the fact. It simply records the outcome.

Tax Strategies: The Tools

Tax strategies are the legal mechanisms designed to reduce your tax bill. These include approaches like S-Corporation elections, the Augusta Rule, income shifting, and maximizing available tax deductions and tax credit opportunities.

These strategies are not loopholes. They are established provisions within the tax code, often used by those who understand how to apply them effectively. However, simply knowing about these strategies does not automatically create savings. Without proper execution, they remain unused opportunities.

Tax Planning: Making It Work

Tax planning is the proactive process that connects everything together. It involves structuring your finances, business entities, and decisions throughout the year to ensure that strategies are implemented correctly and effectively.

This includes setting up the right entity structure, managing the timing of income and expenses, maintaining proper documentation, and coordinating with your CPA and advisory team. Unlike tax preparation, which looks backward, tax planning looks forward and actively shapes your financial outcome.

In simple terms, tax strategies are the tools but tax planning is how and when those tools are used.

Why Most Physicians Overpay

Many physicians operate within a reactive system. They rely on a CPA or tax preparer to file their returns and answer occasional tax questions, but they lack a proactive framework designed to reduce taxes throughout the year.

This gap is where overpayment occurs. It’s not due to negligence or lack of expertise on the part of a CPA, but rather the nature of their role. Most CPAs function as compliance specialists, not proactive strategists.

As a result, many high-income professionals miss opportunities that could significantly improve their financial position.

The Cost of Being Reactive

Consider a physician earning $300,000 annually. Without proactive planning, the full income may be subject to self-employment tax or payroll tax, and key opportunities for strategic tax deductions may be overlooked.

Over time, this leads to a higher overall tax liability and reduces long-term wealth accumulation. While some individuals may eventually face issues such as unpaid tax, IRS tax debt, or the need for tax relief services, the more common outcome is simply paying more than necessary year after year.

Real Example: S-Corp Tax Savings for Doctors

One of the most impactful tax strategies for physicians is the S-Corporation election. Instead of paying self-employment taxes on all income, a physician can split earnings between a reasonable salary and distributions.

The salary portion is subject to payroll taxes, while distributions are not subject to self-employment tax. For a physician earning $300,000, this structure can result in annual savings of $10,000 to $20,000 or more.

However, these savings are only realized when the structure is properly implemented and maintained. This includes running payroll, keeping accurate records, and ensuring compliance with IRS guidelines on reasonable compensation. Without proper tax planning, the strategy can fail or even create an IRS tax problem under scrutiny.

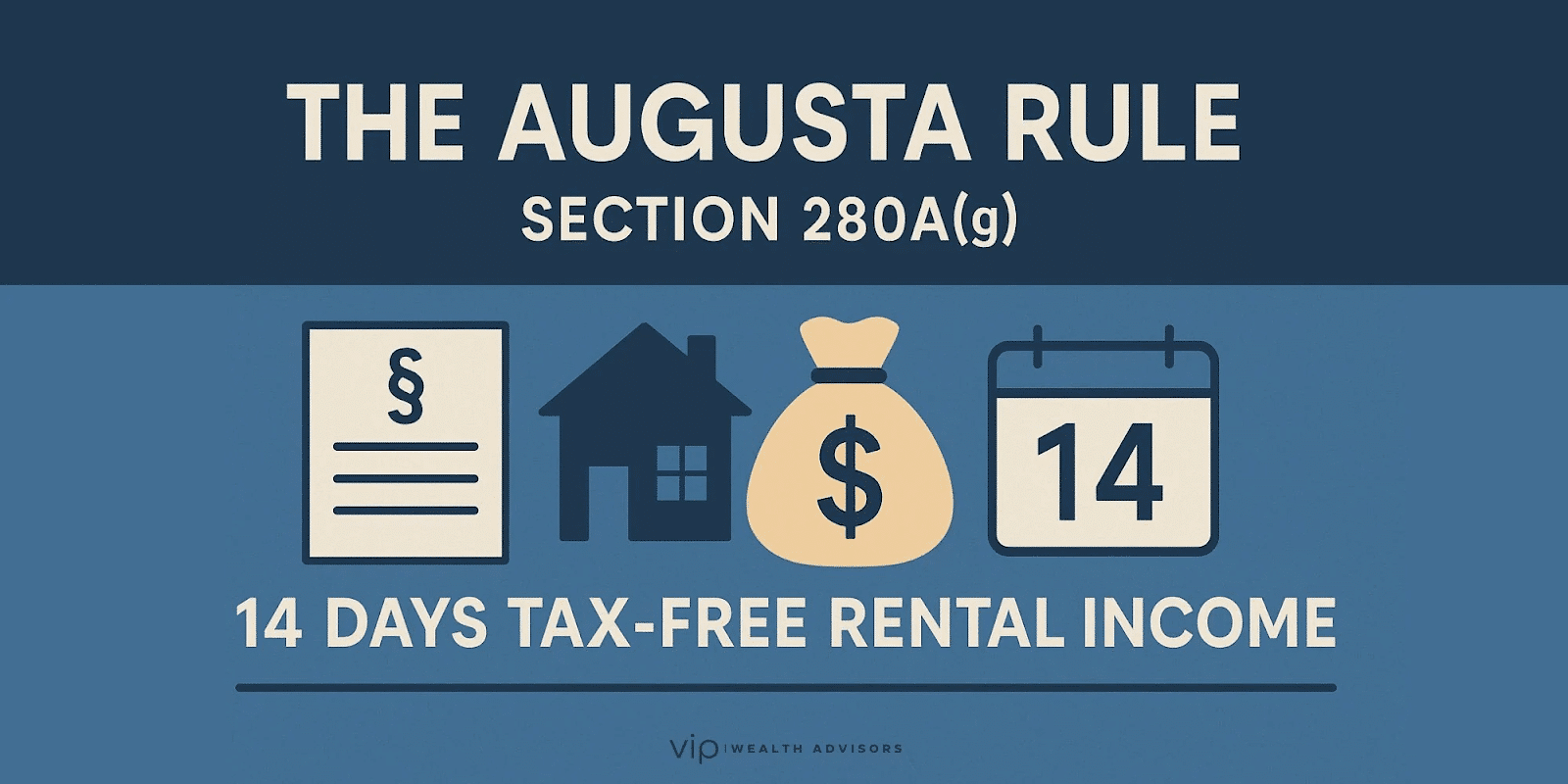

Another Example: The Augusta Rule

The Augusta Rule allows business owners to rent their home to their business for up to 14 days per year. When executed correctly, the business deducts the rental expense, and the individual receives the income tax-free.

This creates a unique opportunity to generate additional deductions while receiving tax-free income. However, it requires proper documentation, legitimate business use, and adherence to fair market rental rates.

Like many strategies, it only works when supported by proactive planning.

Learn More About the Augusta Rule!

You Can’t Fix Taxes After the Year Ends

One of the most important realities in taxation is that once the year ends, your options become limited. At that point, your CPA can file your return, ensure compliance, and assist with tax resolution services if necessary.

But they cannot retroactively restructure your income or implement strategies that were not already in place.

This is why proactive tax planning is essential. It allows you to influence your outcome before it becomes permanent.

The Legally Mine Approach: Keep What You Earn

Legally Mine operates on a simple but powerful philosophy: you should not only earn more you should keep more of what you earn.

Rather than replacing your CPA, the approach is collaborative. Your CPA continues handling tax preparation, while Legally Mine focuses on implementing and maintaining strategies that reduce your tax burden.

This combination ensures both compliance and optimization. It also integrates with broader financial planning, including asset protection and long-term wealth strategies, creating a more comprehensive approach to financial stewardship.

Schedule a Free Consultation Now!

Common Misconceptions

Many professionals hesitate to explore tax planning due to common misconceptions. Some worry about legality, but these strategies are based on established provisions within the tax code. The goal is not avoidance, but lawful optimization.

Others assume these strategies are only for ultra-high-net-worth individuals. In reality, physicians and other high-income professionals are among those who benefit most due to their income structure.

Finally, many believe their CPA is already providing this level of service. In most cases, they are not, not because they lack expertise, but because their role is focused on compliance rather than proactive planning.

FAQs

What is the difference between tax planning and tax preparation?

Tax preparation involves filing your tax return and reporting past financial activity. Tax planning is the proactive process of structuring your finances throughout the year to reduce future tax liability.

Can my CPA help me reduce my taxes, or just file them?

Most CPAs focus primarily on filing and compliance. While some may offer limited planning, proactive and strategy-driven tax reduction typically requires a more specialized approach.

How much can tax planning actually save high-income professionals?

Savings vary based on income and structure, but many physicians see annual reductions of $10,000 to $20,000 or more from strategies like S-Corporation elections alone.

The Bottom Line

If you’re a high-income medical professional, the issue is not whether your taxes are being filed correctly.

The issue is whether you are taking full advantage of the opportunities available to reduce them.

Your CPA ensures compliance.

But compliance alone does not build wealth.

Tax planning does. Because ultimately, it’s not just about how much you earn, it’s about how much you keep.

About Legally Mine

Legally Mine is a leading asset and lawsuit protection company that helps businesses and professionals proactively manage risk. Through specialized consulting and proven legal structures, Legally Mine provides practical tools to protect personal and business assets, reduce liability exposure, and give owners peace of mind, so they can focus on running their business with confidence.